What’s driving the surge in fine white wine trading?

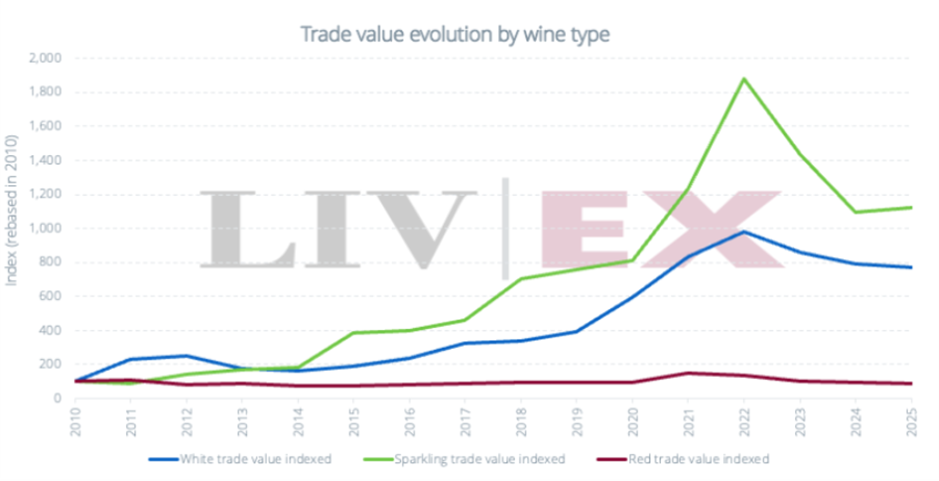

New data from Liv-ex shows that the value of white wine traded on the exchange has soared by 650% since 2010, with Burgundy leading the charge and other regions benefitting from its halo effect. Richard Woodard investigates.

Traditionally, red wine has dominated the secondary market for fine wine, but a structural shift has occurred over the past 15 years, characterised by relative stagnation in red wine trading, alongside a boom in Champagne/sparkling – and, less obviously, a steady uptick in interest in still white wines.

New data from Liv-ex illustrates the extent of this evolution: since 2010, the value of white wine traded on the exchange has soared by 650%, while red wine has dropped by 15%. The surge for Champagne/sparkling over the same timescale is even more dramatic – up 1,100% – but this masks the boom-bust cycle experienced by that segment since 2020. White wines may have experienced a less dramatic peak, but demand has stayed relatively robust during the subsequent market downturn.

If the long-term direction of travel is clear, short-term trends are more elusive. “If you had asked us two years ago, we would have agreed with these findings, that demand for fine white wine was growing,” reports Órlaith Moore Smith, international marketing manager at French auction house iDealwine. “However, our most recent data indicates that the share of white wine sold at auction has stabilised.” The volume share for still, dry white wine at iDealwine auctions dropped to 20.1% in 2025 from 20.8% in 2024, versus 19% in 2023 and 17.7% in 2022.

However you quantify the increase, this is emphatically a story about Burgundy: iDealwine shifted just over 30,000 bottles (scaled to 75cl) of white Burgundy last year, up 13% on 2024, although average hammer prices dropped from €213 to €193 over the same timescale.

At Liv-ex, Burgundy accounts for 69.3% of white wine trading by value in 2026, well ahead of the 10.5% share figure for white Bordeaux, which has suffered a 17.6% decline since 2011. Beyond that, there’s Italy with a 4.5% share, the US at 3.6%, Germany at 3.3%, and the Rhône at 3.2%.

This picture is reflected more broadly in fine wine circles. Geraint Carter, investment specialist at Bordeaux Index, says white Burgundy’s share of the company’s trade by value has increased from about 2% to about 5% over the past decade – which he views in the broader context of a fragmentation in buying patterns, and in particular Bordeaux’s fall from dominance.

Carter adds: “This represents meaningful growth, although it shouldn’t be overstated. Limited volumes, a highly fragmented product/producer base and agency-led distribution naturally cap the extent to which it can feature in the secondary market.”

At Armit Wines, MD Brett Fleming reports: “We have seen significant increases in premium white wines, mostly in line with the Liv-ex findings of Burgundy driving this trend – often the same wine being traded as scarcity increases. I am not sure this illustrates growth, but certainly it shows a trend of premium whites now being traded the same as top-end reds. Given recent volume restrictions from Burgundy in particular, I can only see this increasing.”

Fleming reports persistent interest in Puligny, Le Montrachet, high-end Chablis and Corton-Charlemagne, but points out that “in recent years, you have to also now look at St-Aubin as the quality and demand has radically changed for the better”.

Benjamin Stanley from Armit’s broking department adds: “Meursault is perhaps the one to watch beyond the obvious Montrachet cluster – Coche-Dury in particular commands extraordinary premiums, and the gap between demand and available supply shows no sign of narrowing. Village-level wines from reliable producers such as PYCM [Pierre-Yves Colin-Morey] and Ramonet are also being absorbed faster than before as buyers seek entry points into the category.”

Partner Content

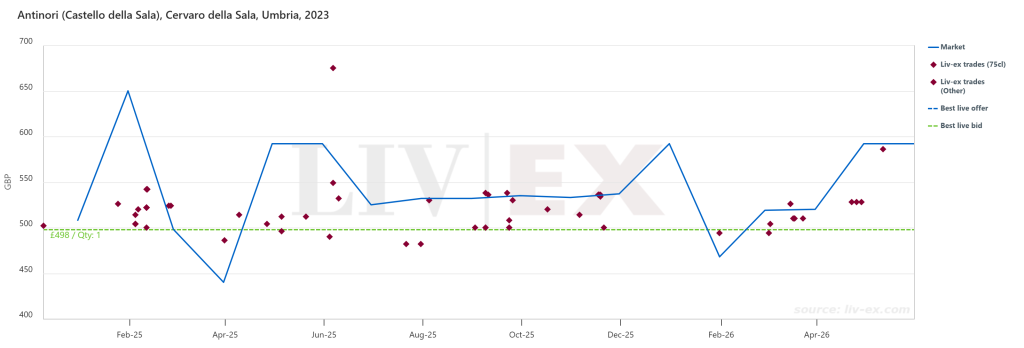

This dynamic of surging demand and restricted supply in Burgundy is beginning to have a ripple effect beyond its borders. Liv-ex market analyst Sophia Gilmour highlights Antinori’s Cervaro della Sala, a Tuscan Chardonnay seldom traded before 2020. So far this year, Liv-ex has seen eight times the volume traded than in the whole of 2019.

Moore Smith ticks off a list of recent non-Burgundy white wine success stories on iDealwine, including a half-bottle of Hermitage Vin de Paille 1989 from Jean-Louis Chave that sold for €576, a bottle of Dagueneau’s Astéroïde Pouilly-Fumé 2000 (€2,066), and a bottle of Keller’s G-Max Riesling Trocken 2021 (€1,440).

Nor is white Burgundy’s secondary market dominance necessarily reflected in primary sales. At The Wine Society, where sales of fine white wines have doubled in the past four years, head of fine wine Alex Turnbull agrees that global demand for white Burgundy has soared, but adds that stock pressures and rising prices have led buyers to look further afield.

“The halo effect of white Burgundy being difficult to secure has been monumental, with regions such as South Africa, Austria, Jura, New Zealand and the Loire really benefitting,” he reports, adding that white Rioja is also in growth. “Even white Bordeaux is making a comeback as members can see that it offers genuine value, with our demand having risen by 55% in four years.” On top of this, The Wine Society’s sales of regional French fine white wines have tripled over the past three years – while fine white Portuguese wines have surged by 370% in four years.

“From the rise of Chenin Blanc in South Africa … to the sheer variety of high-quality fine Italian whites that can be found the length of the country, to small-production cult whites from the USA, such as Ridge’s Grenache Blanc, there have been mini-revolutions within white winemaking around the world over the last decade that really have nothing to do with Burgundy and have had a meaningful impact on consumption,” says Turnbull. “The adage that the finest white wines in the world come from Burgundy simply isn’t true any more.”

At Bordeaux Index, Carter reports a “mixed” picture for white wines beyond Burgundy, explaining: “Sauternes and white Rhône have experienced a long-term decline in trading activity, while there are encouraging signs of growing interest in regions such as the Loire Valley, South Africa and even Germany. Although these categories remain small, they suggest that buyers are becoming more willing to explore beyond the traditional fine wine heartlands.”

Time will tell as to whether, and when, these more granular trends will filter through to the secondary market, but the general expansion and diversification of fine white wine reflects a broader change in consumer sentiment, and how collectors choose to allocate their spend.

For Armit’s Stanley, this structural shift is “real, but nuanced”. He suggests: “There is also a generational dimension: younger buyers entering the market are less anchored to the ‘red wine as status symbol’ orthodoxy that dominated fine wine collecting for decades. The on-trade has played a meaningful role here too, with sommeliers actively championing lesser-known white appellations and driving trial in a way that feeds through to secondary market demand over time.

“Whether this represents a permanent rebalancing or a cyclical correction is the more interesting question – though the supply dynamics in white Burgundy alone suggest the structural case for continued price support is robust.”

Related news

Ancient DNA proves Chianti was once a white wine mecca