Where is the fine wine market heading in 2025?

fine wine monitor – in association with Liv-ex

As the wine world waits impatiently for signs of market recovery, the prospects for the year ahead are mixed – with continued demand-supply imbalances clouding the issue, according to Liv-ex.

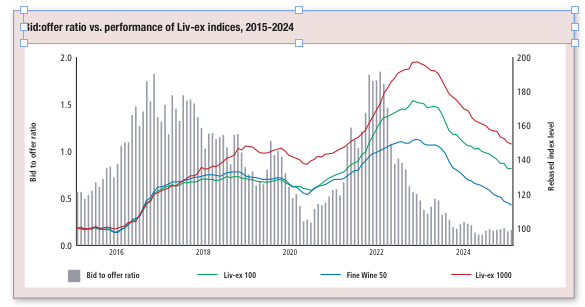

Considering the Liv-ex exchange’s overall bid:offer ratio (as measured by the total value of all bids and offers) alongside the major indices, there exists a clear positive correlation. Drops in the bid:offer have historically predated bearish trend reversals, while increases occur in closer tandem with bullish reversals.

In early 2024, the exchange’s overall ratio dropped to new lows, but recovered slightly towards the end of the year, potentially forming the beginnings of an upward trend. Still, it sits well below 0.5, a threshold we have previously identified as an indicator of price stability.

Since December, the bid:offer ratios of all major Liv-ex Indices – the Fine Wine 50, 100 and 1000, and the Bordeaux 500 – have declined. The vast majority of sub-indices also took hits. The resilient Italy 100‘s ratio rose 0.10 to close with a monthly average of 0.65 – its highest in the past year. The Burgundy 150’s ratio recorded a modest 0.01 increase, but remained one of the lowest at 0.18. All other indices now sit below 0.50.

As we reported in August, Masseto has remained in the lead, with the highest bid:offer ratio of the Italy 100’s component wines. The wine’s ratio has continued to rise (from 1.05 in August to 1.71 this month), and prices have

responded in kind. Of the 10 component vintages, seven have seen month-on-month price increases. Only 20 wines in the Italy 100 are up over a one-year period, and six of these are Masseto. Ornellaia’s bid:offer ratio rose from 0.45 in November to 0.83 in December, and has sustained at 0.79 so far this year. Should demand continue to remain healthy, prices of Ornellaia may also be set to stabilise.

At 0.05, the Sauternes 50 currently has the lowest bid:offer ratio of any Liv-ex index. Given tastes generally moving away from sweet wines, this may not come as a surprise. Even Château d’Yquem, the most frequently traded and highest-value Sauternes on the market, has a current ratio of 0.10.

The Rest of the World 60 follows, with a ratio of 0.16. Given that buyers are expanding the breadth of their purchasing, this may be counter- intuitive. Within the Rest of the World 60, some wines are indeed seeing stable demand. The 10 most recent vintages of Vega Sicilia Unico and Opus One have ratios of 0.59 and 0.47 respectively. Screaming Eagle Oakville Cabernet Sauvignon, Seña and Dominus’ ratios sit vanishingly low at 0.04, 0.05 and 0.06 respectively. Penfolds Grange’s ratio is only marginally better, at 0.10.

fine wine monitor – in association with

Liv-ex is the global marketplace for the wine trade. Along with a comprehensive database of real-time transaction prices, Livex offers the wine trade smarter ways to do business. It gives access to £81m-worth of wine and the ability to trade with 500 other wine businesses worldwide. It also organises payment and delivery through its storage, transportation and support services. Wine businesses can find out how to price, buy and sell wine smarter at: www.liv-ex.com

Related news

Are fine-wine collectors one and the same around the world?

Goedhuis Waddesdon: ‘there is appetite for fine wine among the younger generation’

Fine wine market stabilised during H1 as US buyers 're-engaged'