Auction update: Bordeaux means business

As the fine wine world begins its annual springtime immersion into Bordeaux’s en primeur campaign, iDealwine takes a deep dive into how the region’s top cuvées are performing on the secondary market.

If 2025 is shaping up to be a make-or-break moment for the en primeur system, then it may also be the comeback year for Bordeaux on the secondary market. Far from fading, the region continues to command sustained, if highly fragmented, global demand. Auction data not only highlights which wines are most sought-after, but also reveals who is buying them and how preferences are evolving across key markets. With bidders spanning more than 60 countries, iDealwine’s results provide a compelling lens through which to track these shifting market dynamics.

Blue-chip performance

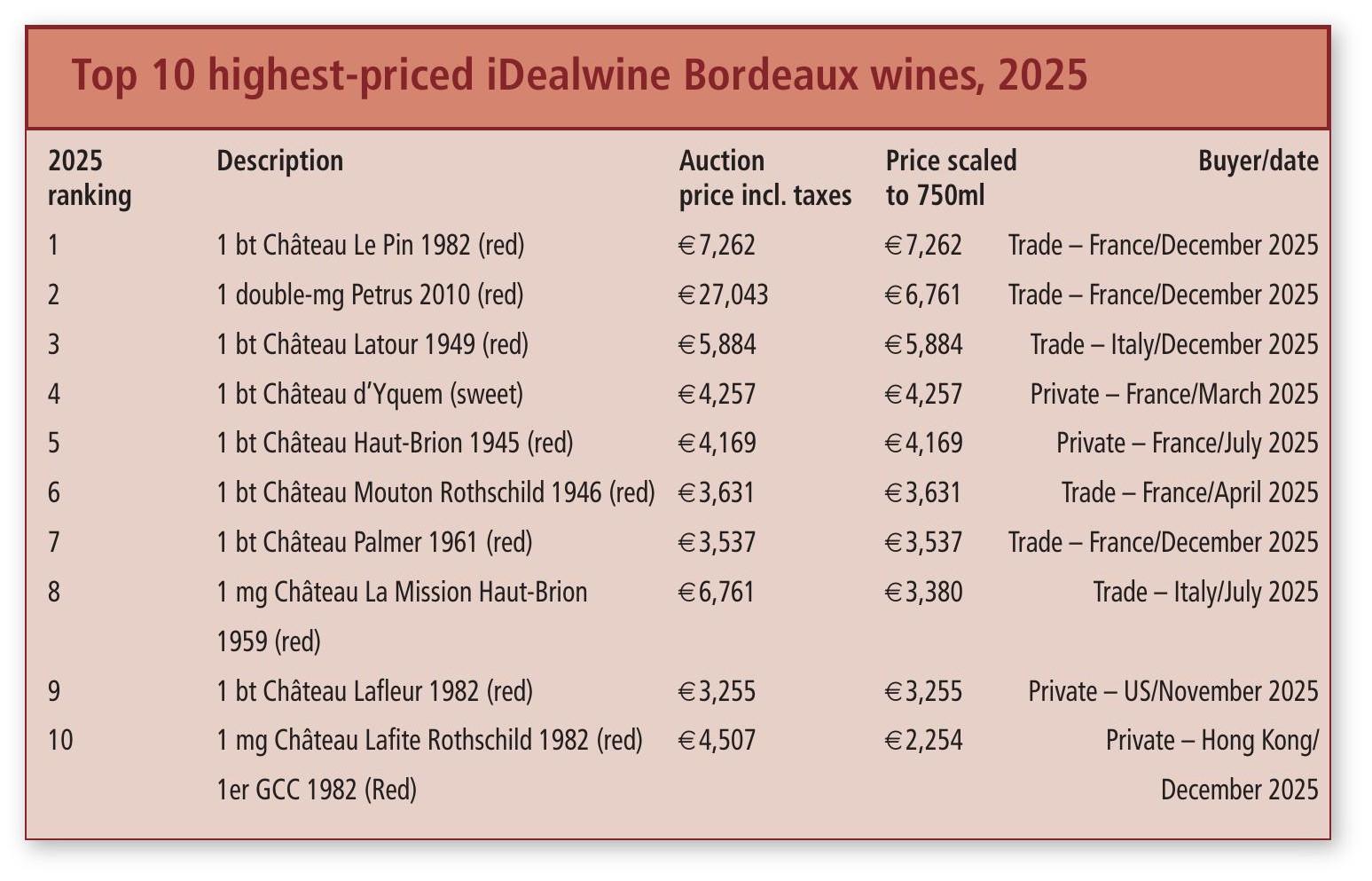

When ranking the top auction results of 2025, as well as the wines that provoke bidding wars and the most sought-after estates (which are all published in iDealwine’s annual Barometer), the data reveals that the established hierarchy remains unchanged from 2024. Petrus, Château Mouton Rothschild and Château Lafite Rothschild continued to dominate in terms of value traded, well ahead of all other properties. Among these true market locomotives, Petrus remained the only property with an average price comfortably above the €2,000 threshold – reaching €2,480 – despite falling volumes (-11%) and a slight dip in its average price (-4%). The five first growths classified in 1855 follow in succession from second to sixth place, underscoring the enduring power of these historic names, both in the imagination of enthusiasts and in the reality of auction results. Château Mouton Rothschild and Château Lafite Rothschild saw a rise in their total value, driven by a sharp increase in volumes, with 1,927 (+33%) and 1,691 (+22%) bottles (when scaled to 750ml) sold respectively in 2025, making them the most actively traded properties of the top 20 in terms of bottle count. More broadly, Bordeaux’s growth has been volume-led. When ranking the top 20 Bordeaux properties that are highest in demand among collectors, a handful of properties stood out, recording striking increases in their volumes, signalling either a resurgence of interest or strong strategic decisions by well-informed investors. Taking two properties involved in significant appellation and ranking changes in recent years – Château Lafleur and Château Figeac – iDealwine has analysed their auction results. Sales volumes of Château Lafleur doubled in 2025 – its withdrawal from the Pomerol appellation seems to have attracted interest from both collectors and consignors. At Château Figeac, meanwhile, there was a sharp rise in the volume (+72%) sold at auction, with only a marginal dip in average price (-3%), confirming the momentum and enduring appeal of this property since its elevation to Premier Grand Cru Classé A status.

Best of the Rest

Looking beyond the first growths and the top 20 ranked Bordeaux châteaux at auction, several properties have recorded particularly sharp growth in value, namely Vieux Château Certan (+141%), Château Canon (+112%), Château Rauzan-Ségla (+91%) and Château Smith Haut Lafitte (+88%). These performances point to a broader re-evaluation of highly sought-after names among bidders. In terms of average price, Château Le Pin sits just behind Petrus at the top of the rankings with €2,417, nicely illustrating the premium consistently awarded to micro-estates in the Pomerol appellation.

Burgundy versus Bordeaux

While Bordeaux’s value share of the auction market has gradually declined in recent years as Burgundy and other regions have gained ground, 2025 suggests a more nuanced picture. Burgundy continues to dominate in major fine wine hubs such as Hong Kong, South Korea and the US. The most recent figures show that, in Singapore, historically a Bordeaux stronghold, buying patterns have evolved, with Burgundy and Bordeaux now on a par, each accounting for 34% of shipped volumes. Across Europe, the narrative is far from one-directional. Italy shows a strong preference for Burgundy, though

Sauternes’ Château d’Yquem remains a notable outlier, rivalling top Burgundy producers in desirability. Germany, another traditional bastion of Bordeaux, saw Burgundy take the lead by value in 2025 (36%), overtaking Bordeaux, which had led by eight points the previous year. However, Bordeaux still leads in volume terms at 34%, underscoring its enduring depth of demand. Switzerland stands out, with Bordeaux commanding 37% of value and 31% of volume – well ahead of Burgundy. Spain has seen a sharp resurgence, with

Bordeaux climbing to 46% of auction value (up from 36% in 2024), dominated by blue-chip names such as Petrus, Lafite Rothschild and Latour. In Scandinavia, Bordeaux has regained the upper hand, accounting for 34% of value and 31% of volume, reversing 2024’s Burgundy-led hierarchy.

Bordeaux Resurgent

iDealwine posted a record performance in 2025, with auction sales reaching €42.4 million, up 9% year-on-year, while volumes surged 19%. Within that growth, a notable shift emerged. Average Burgundy hammer prices softened (down 15%) and, while the same is true in Bordeaux, it was at a much lower rate (-3%). Burgundy still accounts for more than 40% of total auction value, but Bordeaux’s share rose from 27% to nearly 30%. With 105,274 bottles of Bordeaux auctioned in 2025, one in three of all bottles sold came from the region. It may not amount to a seismic shift, but it is a meaningful change – and one that stands in contrast to the persistently gloomy narrative surrounding Bordeaux.

Auction update – in association with iDealwine