Champagne on the secondary market has moved from ‘correction to consolidation’

Champagne prices on the secondary market are stabilising after a rollercoaster few years, underpinned by a shift in buyer sentiment. Richard Woodard reports.

The headline for last year’s article in db’s Champagne Report on the secondary market was ‘Steady as she goes’. After the boom-bust cycle of the first half of the 2020s, the prevailing sentiment at the time in the region was that a little stability in the secondary market wouldn’t go amiss. One year on, those wishes have largely been fulfilled.

“Since a low in August 2025, when the Champagne 50 [index] was down 33.1% since the September 2022 peak, it has risen 1.7%,” reports Tom Burchfield, head of market intelligence at Liv-ex. “So, in short, the picture is one of broad stability in terms of price performance.”

But there are wrinkles: year-to-date (March 2026), 28 components of the index were up, 20 were down and two were flat. “We continue to see new vintages soften post-release, which will continue to drag the broader index down,” Burchfield explains. “But back vintages are generally looking stable.”

This sense of cautious calm pervades auction rooms and wine merchant offices around the world. “In practical terms, we seem to have moved from correction to consolidation,” says Amayès Aouli, global head of wine and spirits at Bonhams. “Prices are significantly more rational than they were two years ago, and that tends to bring collectors back into the market with renewed confidence.”

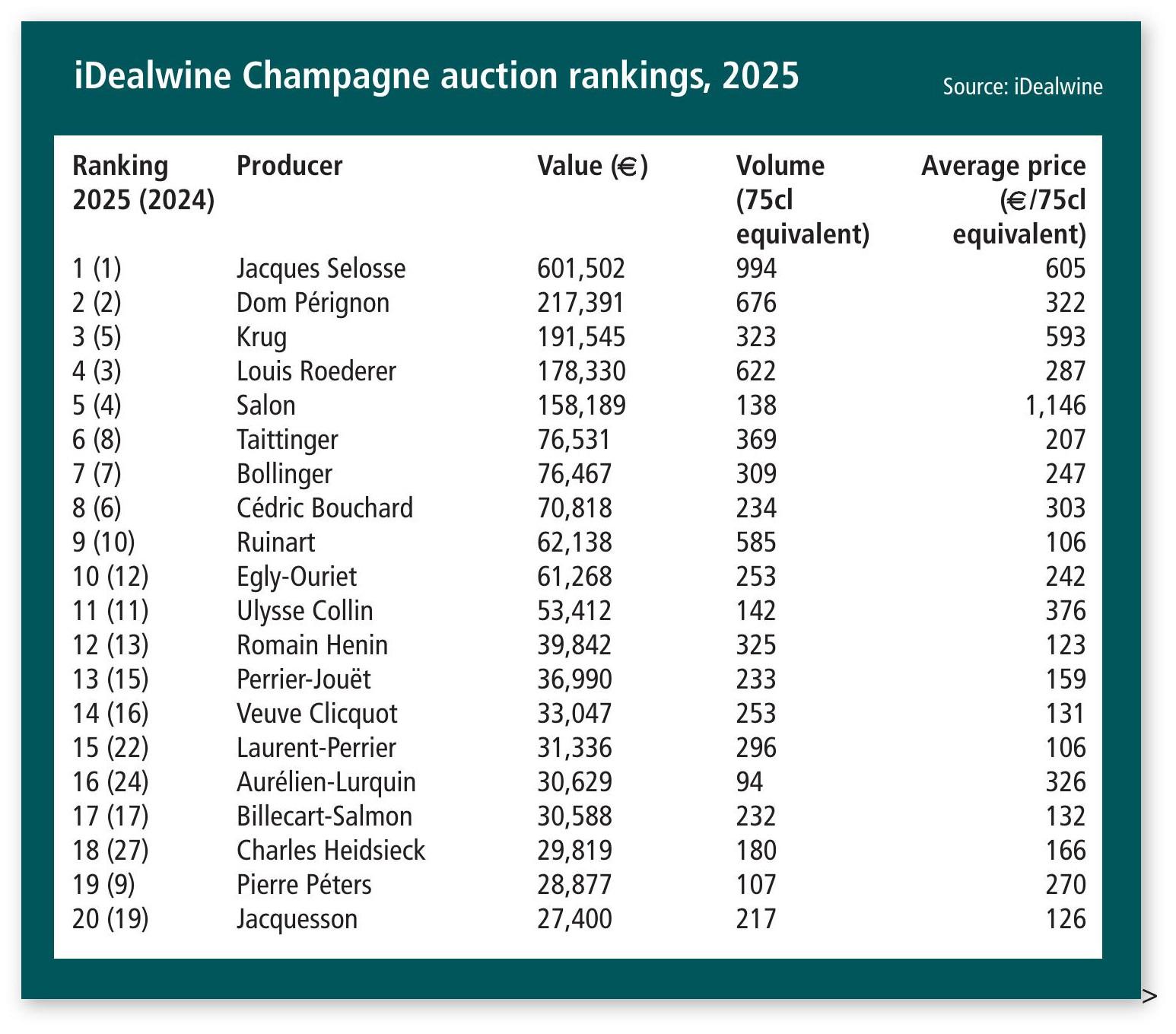

In similar fashion, Órlaith Moore Smith, international marketing manager at iDealwine, highlights the “striking resilience” of Champagne prices in the company’s recent auctions. Volumes remain relatively low, at 13,000 75cl bottle equivalents in 2025, up only 4%, but value rose by 21% over the same timescale. “This means that the average price of Champagne at auction increased in 2025 (+16%), reaching €201 per bottle,” she says.

But, as the Liv-ex numbers imply, any recovery remains tentative and patchy.

“Over the past five to six months, we’ve definitely seen signs of stabilisation,” reports Geraint Carter, of Bordeaux Index’s investment team. “Looking ahead to [the rest of] 2026, the outlook feels flat to me.

“As a generalisation, Champagne has been less volatile than Burgundy, more resilient than Bordeaux, but price performance has not quite been as robust as Italy. It benefits from strong liquidity and genuine end-consumer demand, but given the market backdrop and geopolitical tumult of the past five to six years, some price fluctuation is hardly surprising.”

‘Green shoots’

Giles Burke-Gaffney, fine wine director at Justerini & Brooks, has seen consistent evidence of “green shoots” for Champagne sales in recent months – in line with general market trends – but not enough to encourage any longer-term optimism, especially with the volatile backdrop of war in the Middle East and Ukraine.

“From a broking perspective at Justerini & Brooks, we are seeing a gradual pick-up in client enquiries for Champagne, suggesting confidence is returning, even if pricing has yet to fully respond,” he continues.

This inconsistent performance is further illustrated by the experience of Sotheby’s,where global head of wine and spirits Nick Pegna contrasts the “strong growth” of the 2022 to 2025 period with a less buoyant past 12 months, despite a rally that began in the autumn. But this may relate to the auction’s house’s individual circumstances, he points out.

“Champagne seems to have had a less good year in 2025 versus 2024, with interest reducing as a percentage of the overall sales. This is more to do with a peak for us sourcing mature Champagne in 2024, as well as the overall fine wine pie becoming larger for us.”

Meanwhile, Tim Triptree MW, international director of wines and spirits at Christie’s, detects “clear signs of recovery”, explaining: “We have seen an increase in prices since mid-2025, which is an encouraging shift in sentiment. Demand is being led by mature vintages of prestige cuvées, which are increasingly scarce and difficult to source. Wines such as vintage Krug, Dom Pérignon and Salon remain particularly sought-after,reflecting both their quality and rarity.”

Hard-to-find mature vintages, such as 1982, 1985, 1990 and 1996, vie for attention with more recent standout years, including 2008 and 2012.

This reflects a traditional strength of Champagne in the secondary market, as Aouli explains. “Champagne enjoys a structural advantage that very few collectable assets possess: it is not only collected, but constantly consumed. Every celebration quietly reduces global supply. That natural attrition, combined with a broad international collector base, should continue to support demand for the most desirable cuvées.”

Back vintages

As market conditions have evolved and buyers have become more considered and demanding, the relationship between new releases and back vintages has become increasingly complex. Bordeaux Index’s Carter is blunt. “Recent releases have been more miss than hit,” he says. “While producers obsess over ‘brand positioning’ and have legitimately different time horizons to intermediaries, consumers are perfectly aware of the superior relative value often available on the secondary market. Unless primary pricing reflects not just the cost of capital, but also the scars left by recent market losses, volumes are not going to return to anything like previous levels.”

The issue for producers is that, while demand may have softened, their costs continue to rise. “To some extent, yes, the market has been challenging,” admits Charles Philipponnat. “But our costs, especially that of grapes, being what they are, price cuts have been out of the question. Our strategy has been to hold our own and upkeep our position in all markets.”

Here, aged releases and vinothèque programmes, as well as provenance-rich single-vineyard cuvées, have an increasingly significant presence. Philipponnat has been playing this game since 1935 with Clos des Goisses, and more recently with the addition of Le Léon, La Rémissonne and Les Cintres (from 2006), not to mention Clos des Goisses’ LV programme since 2012. “I consider it a testimony and tribute to Champagne as a ‘grand vin’, much in the same tradition as Burgundy’s ‘climats’,” says Philipponnat.

This view is endorsed by Charles Duval- Leroy, who describes late-release and provenance-driven Champagnes as playing “a key role in demonstrating the extraordinary ageing potential and diversity of the Champagne region”; and by Julie Renault, director of marketing, communication and social engagement at Lanson.

“The current environment is undoubtedly more demanding for Champagne, particularly at the upper end,” she says. “Consumers and collectors today are particularly sensitive to the rarity of wines and to what time alone can offer because, ultimately, time is what creates true value.

“At the same time, we observe a clear shift towards wines with a strong identity, wines that combine authenticity, provenance, precision and the ability to evolve over time … More broadly, these trends reflect a shift towards wines that offer more than quality alone: wines that tell a story, that are rooted in time, and that create a deeper connection with collectors.”

Blurred lines

Provenance-centred releases from major houses also blur the lines between the big names and the growers who have assumed a progressively more influential role on the secondary market in recent years. Both, it’s clear, have their parts to play in the future evolution of the market, but there are signs that interest in growers may have ebbed somewhat.

Moore Smith at iDealwine identifies two notable trends from recent auctions: fierce bidding for collectable vintages including Salon 1955, Dom Pérignon Oenothèque 1964 and Clos des Goisses 1961; and high prices fetched by stellar growers such as Jacques Selosse, Pierre Péters and Cédric Bouchard, although she notes that growers have begun to slip down the iDealwine rankings more recently.

For Charlie Montgomery, BBX trading manager at Berry Bros. & Rudd, the shift towards the reassurance offered by big names is clear. “We have seen that our fine wine marketplace BBX Champagne sales have been dominated by the bigger Champagne houses and prestige cuvées, particularly in the best Champagne vintages,” he explains. “The market share of Champagne has generally grown over the course of the last financial year. We have seen that 2008 is the most popular vintage at 22% of all Champagne sales, with 2008 Dom Pérignon very popular in 2025.”

“High-end growers (Selosse excepted) currently play less of a role than a few years ago,” adds Liv-ex’s Burchfield. “Across the board, we have seen trade focus on tried and tested producers and vintages. While that is true for now, one might expect that, should more confidence return to the market, then there might be a renewed focus on more niche growers.”

At auction, big names and niche growers continue to co-exist happily: Sotheby’s Pegna ticks off a list of dominant top-end producers, including Dom Pérignon, Krug, Cristal, Salon and Taittinger Comtes, but also highlights the “great value” offered by growers such as Gaston Chiquet, Larmandier-Bernier, Egly-Ouriet and Agrapart.

Rare finds

Grower Champagnes lack the volumes of the likes of Dom Pérignon, but scarcity is a virtue in the secondary market, argues Triptree of Christie’s. “Leading grower-producers such as Selosse, Cédric Bouchard and Egly-Ouriet are playing an increasingly important role,” he says. “These wines are in high demand, but due to their smaller production volumes, they appear less frequently at auction, which further enhances their appeal.”

In the longer term, the pantheon of sought-after growers is only likely to expand as market conditions improve. “Outside the firmament of established grower Champagne, there is a new generation of lesser-known growers across the region making wonderful, distinctive, artisan wines that reflect a place, such as Dehours and his Marne Valley Pinot Meuniers, or Pierre Paillard and their Pinot Noirs from Bouzy grand cru,” says Burke-Gaffney of Justerini & Brooks.

“There is also relative value to be found amongst some of the leading houses – those that offer a more compelling entry point for collectors prepared to take a medium-term view, particularly where quality and track record remain strong, such as Philipponnat.”

Upbeat outlook

Challenges persist for Champagne on the secondary market, but the mood music has become decidedly more upbeat in the past six months or so; Triptree believes value can now be found in more recent vintages such as 2014 and 2015, where volumes are relatively good and pricing now more realistic, with the prospect of appreciation as the market strengthens. Burchfield points to some instances of pricing restraint, highlighting Krug 2014 and Dom Pérignon 2017, adding: “This is of course welcomed and shows producers looking to support their merchant partners.” What is more, there are wines that have reached pricing stability and, while hardly cheap, offer relative good value – including Cristal 2015 and Salon 2012.

Perhaps most importantly, there’s a sense of a virtuous circle taking shape, where quality levels are consistently high, and collector appreciation is pursuing a similar upward trajectory.

“Paradoxically, for all the gloom, there has never been a better time to be a Champagne drinker,” says Carter of Bordeaux Index. “Wines such as Bollinger PN, Taittinger Comtes and Philipponnat 1522 (to name but a few), alongside top growers, offer fabulous absolute value, and with wonderful vintages like 2012/2013/2014 plentiful in the market (with 2018 in the pipeline), there is something of an embarrassment of riches.”

Burchfield of Liv-ex agrees. “Champagne’s shift towards greater sustainability, its growing reputation as a more vinous wine rather than just a celebratory one, and its emphasis on uniqueness should all put it in good stead when you combine it with its formidable brand power,” he says.

Unique structure

Part of this is down to Champagne’s unique structure, according to Montgomery of Berry Bros. “With red and white wines, buyers face an enormous range of producers and regions,” he points out. “[With Champagne], there is a simplicity in the smaller number of producers, a fairly simple hierarchy of cuvées (NV, vintage, prestige) and it is relatively easy to understand the best recent vintages – plus there is also a good degree of availability in these wines.

“All this makes for a much more accessible category, particularly for those who are newer to buying in the secondary market, who are likely to have a degree of understanding of Champagne already.”

Aouli closes with an anecdote from a recent Bonhams auction of the first three bottles released from Barons de Rothschild’s single-vineyard cuvée, Le Grand Clos. He explains: “They achieved £16,000, with all proceeds donated to charity – a remarkable debut that reflects the appetite collectors now have for rare and distinctive Champagne. In short, Champagne is becoming not only celebratory, but intellectually compelling.”

Related news

How Champagne mastered the art of the collaboration

How Yvonne Seier Christensen forged her own path in Champagne