No and low alcohol drinks category continues to grow, reaching US$10billion in value

As consumers embrace dry January, new research reveals that no- and low-alcohol drinks continue to grow in popularity. But what is next for the category as we head further into 2022? The drinks business investigates.

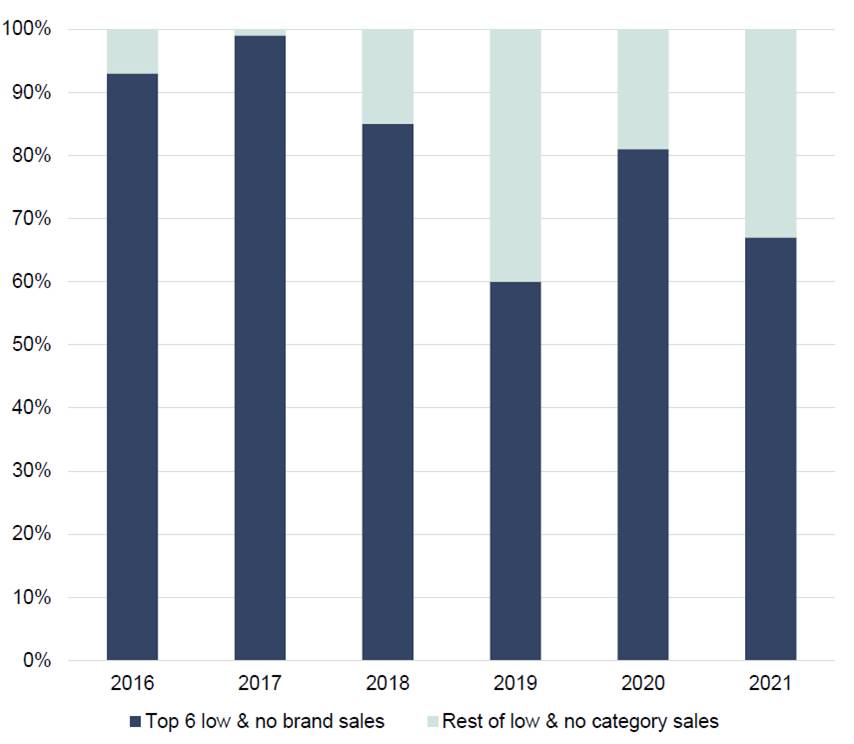

Once a rarity in the global beverage alcohol market, no- and low-alcohol drinks grew by more than 6% in volume in 10 key global markets in 2021, and now command a 3.5% volume share of the industry, according to a new study published by IWSR Drinks Market Analysis.

And the trend has really taken off in the last few years, with the market value of NoLo drinks up to almost US$10 billion in 2021 from US$7.8 billion in 2018.

The IWSR forecasts that no- and low-alcohol volume will grow by 8% CAGR between 2021 and 2025, compared to regular alcohol volume growth of 0.7% CAGR during that same period.

“While January has become a popular month for people to cut back or abstain from alcohol, interest in no- and low-alcohol drinks has increasingly become a year-round trend among consumers across the world,” says Emily Neill, COO of IWSR Drinks Market Analysis.

“To meet that demand, beverage alcohol companies have invested heavily to introduce a number of innovative new products, and many established mainstream brands have recently crossed over to develop no/low alcohol versions of their popular beer, wines, and spirits.”

Indeed, well-established brands are joining the fold, creating alcohol-free alternatives to their popular offerings. The latest to tap into the trend is Italian company Martini and Rossi.

With 58% globally drinking more non-alcoholic and low-ABV cocktails than a year ago, according to the 2022 Bacardi Cocktail Trends Report, demand for premium NoLo options are expected to continue growing.

Martini and Rossi has introduced two non-alcoholic vermouths, Floreale and Vibrante, in a bid to appeal to mindful drinkers.

New, strictly NoLo brands are also trying their luck with consumers, and fairing well. Atopia, a new 0.5% ABV spirit was created by William Grant & Sons master distiller Lesley Gracie. Last year, Waitrose saw a 60% increase in sales of Atopia in the 52 weeks before 4 December 2021, according to Nielsen MAT data.

Wine and spirits supplier Enotria & Coe described NoLo drinks as the current biggest growth category. The supplier’s sales of no- and low- products was up 70% in 2020, and up a further 35% in 2021.

By contrast, Enotria & Coe’s sales of still wine in 2021 were 73% of comparable sales in 2019, as the pandemic continues to create challenges for the category as a whole.

Partner Content

Zippy Bakowska, head of customer marketing at the supplier, told db: “We can see particular growth in low and no RTDs and products in sustainable packaging. There seems to be a strong correlation between the adventurous consumer profile who is interested in both of these product trends.

Led by younger, more health-conscious consumers, the trend towards moderate drinking patterns has boomed in the last few years. From 2014, Enotria & Coe’s no- and low- listings have grown from 1 product to a total of 112 in 2021.

Alcohol Change UK’s Dry January campaign began as a public health initiative in 2012. Dr Richard Piper, the charity’s CEO, told db he was “proud of our success in driving the demand” for NoLo drinking options, noting his own personal choice to avoid alcoholic drinks altogether in favour of no- and low- options.

“It’s now up to the industry to meet that with supply. It’s taken time, but it has started to do that” he added.

Alcohol Change UK also provides reviews of NoLo alternatives on its website. Traffic to these articles has boomed in recent years, from 100,000 page views in 2018 to an estimated 500,000 in 2021.

“That’s a five fold increase in people looking at and reading those reviews. And that’s, that can’t just all be the same person. That’s powerful growth and increasing people, and we genuinely take some credit,” Piper said.

As we move towards the end of January, and many people’s month of sobriety comes to an end, how will the NoLo trend continue in 2022?

Piper remains hopeful. “Dry January is the start of a journey for people,” he said. “For many people that’s when it really gets going, because that’s when they start taking big decisions.”

Indeed, this transition is reflected in NoLo sales throughout the year.

Enotria & Coe’s historic sales data of no- and low- products does not suggest that Dry January is necessarily the dominant consumption period for this category.

“There is certainly a lot of noise about this category in Q1, but sales are more evenly spread throughout the year than media coverage would suggest,” Bakowska said.

Looking at the figures for 2021, Q1 accounted for 7% of the company’s no- and low- sales in that year, with Q2 accounting for 21%, Q3 for 31% and Q4 for 40%.

In light of this, the end of January is unlikely to mean the end of moderate drinking, with more and more consumers being turned on to brands offering low-ABV alternatives. And with a predicted volume growth of 8% CAGR by 2025, the trend shows no signs of slowing.

Related news

Maison Sichel: ‘Brexit has been an opportunity’

94% of alcohol-free beer drinkers also consume booze

IWSR: 2035 will be 'vastly different' for the global drinks sector